What Revenue and Risk Tell Us About Salesforce

Stock Price Isn’t Business:

When people talk about tech stocks, the conversation usually starts and ends with stock price. Is it up? Is it down? Did it beat the market?

But stock price alone is a poor proxy for the health of a business and an even worse proxy for strategic risk.

To understand where Salesforce really stands, you have to look at revenue, valuation, and competitive positioning together.

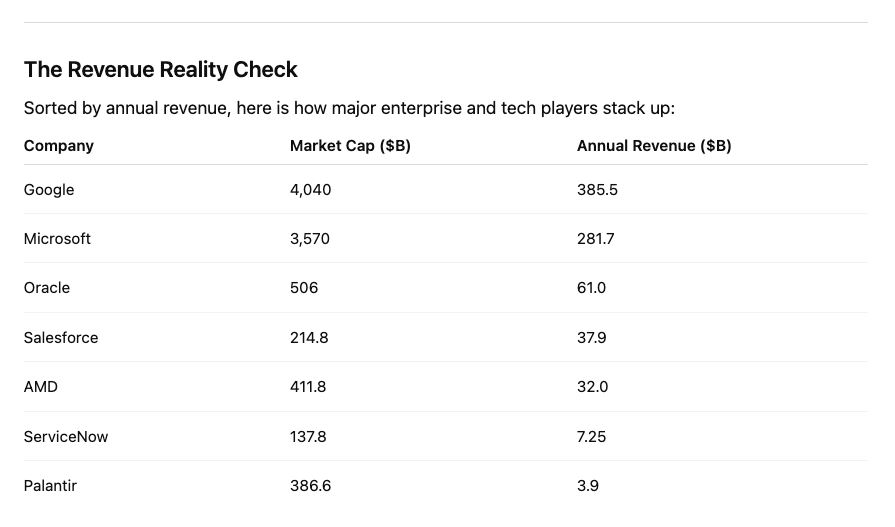

The Revenue Reality Check

Sorted by annual revenue, here is how major enterprise and tech players stack up:

Salesforce generates more revenue than AMD, over five times the revenue of ServiceNow, and nearly ten times the revenue of Palantir. Yet its stock performance often paints it as a laggard.

That disconnect creates questions. Some are fair. Some are overstated.

Salesforce’s Business Health Versus Its Stock

From an operational standpoint, Salesforce is solid.

It generates roughly $38 billion in annual recurring revenue, maintains extremely high customer retention, and is deeply entrenched in enterprise operations. Its platform spans sales, service, data, and AI, and recent cost discipline has improved operating margins.

This is not a company in decline.

So why does the stock feel fragile?

The Real Risk: Valuation Compression, Not Business Erosion

Salesforce’s primary stock risk is valuation compression rather than revenue collapse.

It occupies a difficult valuation position. It is too large to command hypergrowth SaaS multiples, too enterprise-focused to benefit from consumer or AI-driven hype cycles, and not large enough to enjoy the index gravity of mega-cap companies like Microsoft or Google.

As a result, Salesforce’s stock is more exposed to macroeconomic conditions, interest rate sensitivity, and short-term earnings narratives. These are market risks, not competitive failures.

Does a Weaker Stock Open Salesforce to Competitors?

Not in a meaningful way.

Salesforce’s competitive moat is operational rather than financial. Customers are locked in through multi-year contracts, deeply embedded CRM data, complex enterprise implementations, and high switching costs. Revenue teams often rely on Salesforce as a core system of record.

Competitors do not win Salesforce customers because Salesforce’s stock is underperforming. They win only when Salesforce overprices, overcomplicates its product, or fails to execute.

Stock performance does not materially change that dynamic.

M&A or Takeover Risk: Real or Overstated?

This concern surfaces whenever a large company underperforms the broader market.

A hostile takeover is highly unlikely. Salesforce still commands a market cap above $200 billion, generates strong free cash flow, and has governance structures that discourage activist pressure at that scale.

A strategic acquisition is even less plausible. There are very few companies capable of acquiring Salesforce operationally or politically. Microsoft would face severe regulatory barriers. Google would struggle to justify product overlap. Oracle would face cultural and strategic friction.

Salesforce acting as an acquirer remains more realistic than Salesforce being acquired. In fact, stock underperformance has pushed the company toward greater discipline, fewer large acquisitions, and stronger focus on margins and integration.

The Subtle Risk: Narrative Drift

The most credible risk Salesforce faces is not takeover or competition but narrative erosion.

If Salesforce becomes framed as legacy SaaS, as a CRM rather than a platform, or as stable but unexciting, perception begins to lag reality. That affects talent attraction, partner momentum, and how innovation is valued by the market.

This makes storytelling a strategic imperative. Salesforce must consistently articulate why its platform remains essential, why its data advantage is difficult to replicate, and why AI embedded in CRM workflows is structurally differentiated.

Final Take: Undervalued, Not Under Threat

Salesforce’s stock performance reflects market fatigue with enterprise SaaS, preference for fast-moving narratives, and short-term valuation psychology.

It does not reflect weak fundamentals, competitive collapse, takeover vulnerability, or structural decline.

Salesforce remains a core enterprise infrastructure company. The risk is not that it gets acquired. The risk is that the market temporarily forgets how difficult it would be to replace it.

Over time, markets tend to rediscover that reality. When they do, stock prices usually follow the business rather than the other way around.